In last month’s update, I was unable to provide a forecast because China continued to battle COVID, Joint Comprehensive Plan of Action (JCPOA) negotiations were still unresolved, the market belief that the Fed will increase rates aggressively, Europe was considering sanctioning Russian oil, and the war in Ukraine continuing to rage. While all these factors continue to be true in varying degrees, the market appears to be acclimatizing itself to this new, harsh environment.

My forecast is that West Texas Intermediate (WTI) oil price will range between $110 to $130 per barrel during the month of June. With inflation in the high single digits in Europe and the US, central banks are determined to raise rates. During the past month, stocks have been volatile and were down significantly before rebounding in late May. Even as I write this post, the VIX is hovering around 26 percent, which is high. If the economy continues to struggle with interest rate increases, oil prices may fall in sympathy with other financial assets. On the other hand, as Europe continues to reduce its dependence on Russian oil and gas, oil prices may well go higher. On balance, I am more concerned about oil prices surpassing the high end of my range than the lower end because I expect the oil market to continue to tighten.

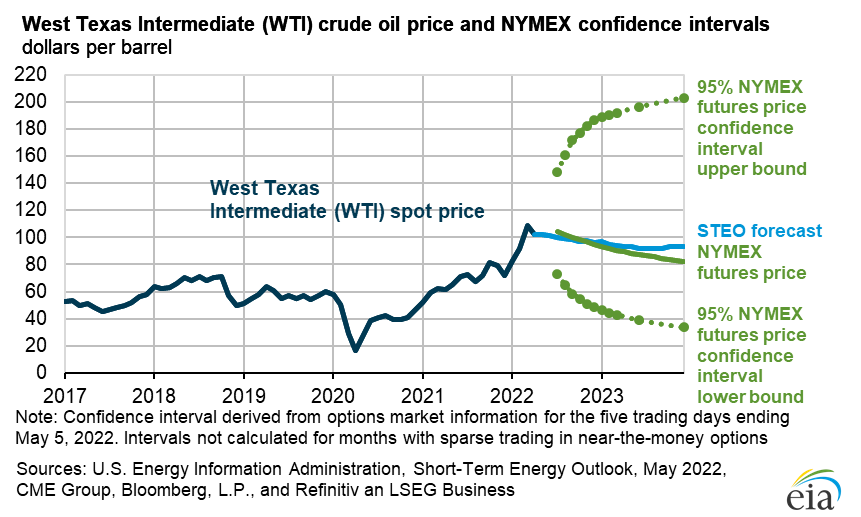

Some might be inclined to think that a $20 price range forecast is excessive. When oil prices were in the $60s, I gave a $10 price range. Now that oil prices have roughly doubled and in a continuing uncertain geopolitical and economic environment, assuming no major events that might cause an oil price shock in either direction, I am comfortable with a $20 price range. Also, the U.S. Energy Information Administration’s “Short-Term Energy Outlook” released on May 10 similarly used a reasonably wide range.

EIA May 2022 Short-Term Energy Outlook Oil Price Confidence Intervals

On the topic of inflation, in a May 30 op-ed article (subscription required) in the Wall Street Journal, President Biden stated the following:

First, the Federal Reserve has a primary responsibility to control inflation. My predecessor demeaned the Fed, and past presidents have sought to influence its decisions inappropriately during periods of elevated inflation. I won’t do this. I have appointed highly qualified people from both parties to lead that institution. I agree with their assessment that fighting inflation is our top economic challenge right now.

Second, we need to take every practical step to make things more affordable for families during this moment of economic uncertainty—and to boost the productive capacity of our economy over time. The price at the pump is elevated in large part because Russian oil, gas and refining capacity are off the market. We can’t let up on our global effort to punish Mr. Putin for what he’s done, and we must mitigate these effects for American consumers. That is why I led the largest release from global oil reserves in history. Congress could help right away by passing clean energy tax credits and investments that I have proposed. A dozen CEOs of America’s largest utility companies told me earlier this year that my plan would reduce the average family’s annual utility bills by $500 and accelerate our transition from energy produced by autocrats.

…

Third, we need to keep reducing the federal deficit, which will help ease price pressures. Last week the nonpartisan Congressional Budget Office projected that the deficit will fall by $1.7 trillion this year—the largest reduction in history. That will leave the deficit as a share of the economy lower than prepandemic levels and lower than CBO projected for this year before the American Rescue Plan passed. This deficit progress wasn’t preordained. In addition to winding down emergency programs responsibly, about half the reduction is driven by an increase in revenue—as my economic policies powered a rapid recovery.

Regardless of one’s political leaning, we can all feel the effects of inflation. How successful politicians and central banks will be in fighting inflation without causing a recession remains to be seen.

As the West continues to take action against Russia, I expect oil and gas markets to continue to tighten. As mentioned in the May 31 article (subscription required) “EU’s Ban on Russian Oil Adds Stress to Region’s Economies” in the Wall Street Journal, Europe is taking active steps to reduce its dependence on Russian oil.

The European Union is set to impose its toughest sanctions yet on Russia, banning imports of its oil and blocking insurers from covering its cargoes of crude, officials and diplomats say, as the West seeks to deprive Moscow of cash it needs to fund the war on Ukraine and keep its economy functioning.

The sanctions, which are expected to be completed in the coming days, are harsher than expected. The ban on insurers will cover tankers carrying Russian oil anywhere in the world. These sanctions could undercut Russia’s efforts to sell its oil in Asia. European companies insure most of the world’s oil trade.

The embargo is a high-risk strategy for the EU, forcing the bloc to break its dependency on cheap Russian energy. It is likely to fuel inflation already running at the highest pace in decades on both sides of the Atlantic.

Just as I was drafting this article, the Wall Street Journal reported (subscription required) in an article titled “OPEC Weighs Suspending Russia From Oil-Production Deal” that some OPEC members are exploring Russia’s participation in an oil-production deal.

Some OPEC members are exploring the idea of suspending Russia’s participation in an oil-production deal as Western sanctions and a partial European ban begin to undercut Moscow’s ability to pump more, OPEC delegates said.

Exempting Russia from its oil-production targets could potentially pave the way for Saudi Arabia, the United Arab Emirates and other producers in the Organization of the Petroleum Exporting Countries to pump significantly more crude, something that the U.S. and European nations have pressed them to do as the invasion of Ukraine sent oil prices soaring above $100 a barrel.

Russia, one of the world’s three largest oil producers, agreed with OPEC and nine non-OPEC nations last year to pump more incrementally more crude each month, but its output is now expected to fall by about 8% this year. It couldn’t be determined whether Russia would agree to an exemption from the deal’s production targets.

As the news broke, oil fell from about $117.50 per barrel to about $114 and then rebounded to about $115. My guess, however, is that OPEC will try to take steps to prevent oil prices from suddenly spiking higher but will not attempt to drive prices lower. This development bears watching closely.

Helima Croft retweeted her interview with CNBC:

Oil taking a leg lower this afternoon after reports that OPEC may suspend Russia from its oil production deal.

RBC's @CroftHelima gives us her take on the headline pic.twitter.com/r08XS5yh8v

— CNBC's Closing Bell (@CNBCClosingBell) May 31, 2022

After the initial headline shock from the Wall Street Journal, I expect oil prices to recover.

As stated, my forecasted range of $110 to $130 per barrel is based on the current environment continuing without any major shocks. If the economy worsens faster and more severely than expected or the war takes a sudden turn, then, of course, all bets are off.

Switching topics, I just finished reading a book (Amazon affiliate link) Oil Leaders: An Insider’s Account of Four Decades of Saudi Arabia and OPEC’s Global Energy Policy (Center on Global Energy Policy Series) by Ibrahim AlMuhanna. For those who believe that the oil markets are perfectly rationale and predictable, this book debunks that theory. AlMuhanna mentions that there are important players who can influence the oil markets:

In my opinion, six important players are able to influence market direction, one way or another:

- International business media, particularly specialized energy publications. It is not only what is reported but also the way events are reported, such as the people who are quoted, the news headlines, and news alerts.

- Oil experts and analysts, whether independent or part of a large organization. IHS Markit and PIRA Energy Group, for example, interpret events and information and predict the direction of the oil market and oil prices, which influences the futures market.

- International energy organizations, especially the International Energy Agency (IEA) and OPEC. These information warehouses publish monthly reports about the international oil market that are widely quoted, and their estimates on supply and demand and commercial stocks influence the oil market and its behavior.

- Hedge funds and commercial banks. These players take positions in the oil futures market (long and short), expecting high or low oil prices. Their positions are based on their own in-house information and analysis as well as information from public and private oil officials and experts.

- Government officials from major oil-producing and oil-consuming countries. Whether speaking publicly or privately, what they say can, and does, have a strong influence on the direction of oil prices, especially when inside information or new policy trends are discussed.

- Major oil companies (national or international), including oil trading companies. Most of these companies have extensive internal analyses but do not like to discuss the oil market publicly. They don’t want to be quoted, nor do they typically reveal their information, expectations, and position in the market. Nevertheless, when their information is leaked or given to a limited number of people in a confidential way, they can influence the market and its direction.1

If you are interested in the oil markets, I recommend Oil Leaders.

1Ibrahim AlMuhanna, Oil Leaders (Center on Global Energy Policy Series) Kindle Edition (New York: Columbia University Press, 2021), 228-229 ↩